That’s what it sounds like some Portland voters are saying when they voice support for Measure 26-260 to maintain the city’s parkswith a five-year levy that would increase the rate of taxation from 80 cents to $1.40 per $1,000 of assessed value, a massive 75% increase.

What business would reward a division’s mismanagement and profligacy by giving it more money?

What citizen would tolerate giving more money to a bureaucracy that has consistently failed in its mission while boosting its employment ranks? In 2020, Portland Parks and Recreation had 566 full-time employees. As of January 31, 2025, it had 792 full-time employees, almost a 30%increase. Good grief.

What voters already burdened with absurdly high taxes in an uncertain economy would purposefully burden themselves even more? What voters are unconcerned about the Legislature passing the $4.3 billion gas tax/wage tax bill Governor Kotek is eventually going to sign, particularly when, as numerous economists are observing, folks at the top part of the income and wealth distribution are doing fabulously well, but the other 80% are getting worried.

According to the Tax Foundation, an independent, nonpartisan non-profit research think tank, Portland residents already face some of the highest taxes in the country. “City, county, regional, and state taxes on individual and both net and gross business income combine to create a crushing tax wedge, yielding some of the highest marginal rates on wage income nationwide,” the Tax Foundation says.

What citizen would reward a bureaucracy that, according to a fiscal management audit released on Oct. 15 by the Portland City Auditor’s Office, “…has not taken a systematic approach to finding and implementing cost-saving, revenue-generating or service-reduction strategies.”

Then again, Portland voters have a history of tolerance for, even endorsement of, ineffective government.

In a May 2025 special election, Portland voters, ignoring cautionary arguments, supported Measure 26-259, a $1.83 billion bond to completely rebuild or renovate three high schools, the largest school bond in Oregon history, ignoring projections that there won’t be nearly enough students to fill them. The Oregonian also reported that the new schools would be three of the most expensive high schools ever built in the United States.

The massive spending will also result in space for 15,300 high school students, while Portland State University’s Population Research Center projected in July 2024 that the Portland School District will only have about 10,700 students by 2039.

The last thing Portland needs now is another irresponsible spending measure. Vote NO on Measure 26-260.

On one side you have a phalanx of Democrats proposing the ludicrous idea of paying strikers unemployment benefits, which would make Oregon the only State in the country to grant unemployment benefits to striking public and private sector workers.

Not to be outdone in making nonsensical proposals, now you have a raft of Republicans, mimicking President Trump, proposing that the state forego taxing tips.

Here’s a tip – exempting tips from state taxes is a bad idea.

In their determination to position themselves as supporters of the working man (and woman), 21 of Oregon’s House Republicans have proposed a bill, HB 3914, to end taxation of tips, which are generally perceived as discretionary payments determined by a customer that employees receive from customers.

As written, the bill would not count “service charges” as tips. A restaurant, for example, recently added an automatic service charge equal to 18% of my bill. Even if that was intended to cover for a “no tipping” policy, it would be part of the server’s wages because it was not discretionary.

The 129-word Oregon bill gets right to the point, “There shall be subtracted from federal taxable income any amount of tips properly reported as wages on the taxpayer’s federal income tax return.” That would automatically subtract tips from taxable income in Oregon, too.

The bill deserves a quick death.

According to the IRS, “All cash and noncash tips received by an employee are income and are subject to Federal income taxes. All cash tips received by an employee in any calendar month are subject to social security and Medicare taxes and must be reported to the employer.” So, tip income is taxable income.

Charges automatically added to a customer’s check by an employer and subsequently distributed to employees are not tips; they are “service charges”. These service charges, which are appearing more often on Oregon restaurant bills, are non-tip wages and are subject to Social Security tax, Medicare tax, and federal income tax withholding.

Many consumers think the expanding pressure on customers to leave tips is already out of hand. A no tax on tips policy would likely expand the use of tipped work even further, potentially leading to consumers being asked to tip on virtually every purchase everywhere.

A New York Times article about tipping generated a lot of comments, many of which lamented the seeming spread of tipping expectations to multiple businesses and regardless of the amount of actual service by an employee. “Collectively, we cringe when the iPad is swiveled into our face at the coffee counter or deli; we know it is extortion rather than appreciation for services rendered,” said one person.

There’s also a sense that some businesses are customizing the tip configuration on screen to exploit customers. Most people tip between 15-20%. If you buy a $2.85 espresso and the screen offers 15%, 20% and 25% tip options, you are likely to hit 15%, generating a tip of 43 cents. If a business wants to jack that up, however, it can give you $1, $2, or $3 options on purchases below $10, instead of a percentage. If you pick $1, you have paid a 35% tip. Devious, but effective.

Despite the massive increase in tipping expectations in recent years at multiple businesses, tax experts say a relatively small share of the workforce depends on tips. Only about 2.5% of American workers are in occupations that depend on tips, according to the IRS. Among those workers, 37% earn less than the federal standard deduction. So, they already don’t have to pay federal income taxes.

Other tipped workers benefit from the earned income tax credit (EITC) and/or child tax credit (CTC) to the extent that they don’t have any federal income tax liability. In addition, because tipped workers would keep more of their income, employers could use this law as a justification for lowering workers’ base pay if it is currently above the minimum wage.

In fact, exempting tips from taxation can actually lead to situations where low-income workers end up effectively losing income through losing eligibility to tax credits such as the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC).

The Budget Lab at Yale, a non-partisan policy research center, estimates that less than 3 percent of families would benefit from a broad-based income tax deduction for tips in 2026, but it would still cost the federal government more than $100 billion over the next decade. Restricting eligibility to workers in the leisure and hospitality industries would reduce the cost by more than 40 percent, but that would still leave a big hit on the deficit unless taxes were raised elsewhere.

Even the liberal Oregon Center for Public Policy opposes the no tax on tips idea.

In October 2024, Daniel Hauser, Deputy Director of the Center, said that ending taxes on tips “makes the tax system less fair” because workers receiving tips would get a tax break, but not low-paid workers in general.

If you have two workers, one a bartender who earns about $10,000 of his $40,000 annual income in tips and the other a warehouseman who makes all of his $40,000 income in wages, it wouldn’t make sense to give the bartender a tax break but leave the warehouse worker hanging out to dry, Hauser argued.

It also “creates openings for people to think about, how can my income be categorized as a tip and get this tax break too?,” Hauser wrote. Third, he said, “if the goal is to help the economic security of low-income workers, it’s not very effective…and there are much better ways for us to try and help low-income families in Oregon.”

State Senator Jeff Golden wrote an Opinion column in The Oregonian recently calling for diversion of the next kicker, recently forecasted to be $1.8 billion, to a dedicated Wildfire Programs Fund, which the state treasurer would invest.

It’s just one more way for a hungry Democrat-run government to raid your pocketbook.

The idea came out of a workgroup of 36 stakeholders chosen by Gov. Tina Kotek to deliberate over alternative funding sources for dealing with wildfires.

The key options identified were:

Kicker Funds: One-time use to “jump-start” wildfire funding.

Bottle Bill Adjustment: increase the bottle deposit to include a non-refundable portion for wildfire funding.

Insurance retaliatory tax – Dedicate a portion of existing retaliatory taxes paid by out-of-state insurers to the State.

Ending Balance: Dedicate 0.5% of previous biennium’s appropriations (if there is an ending balance) to the Wildfire Fund.

One time transfer from the Rainy Day Fund (RDF) – directed to wildfire.

Lottery Funds – Constitutionally dedicate a portion of lottery funds for wildfire.

Landowner assessment rates and existing structure – will be part of the solution.

The proposal to create a Wildfire Programs Fund “stands out from the others,” Golden wrote.

“Funding for our programs would come not from the $1.8 billion principal—that would be preserved – but rather from the investment interest it earns.,” Golden wrote. “Assuming 5% annual return (a reasonable guess judging by the Treasury’s investment history), the fund would annually generate $90 million – $180 million each biennium – for wildfire programs. While that’s not enough to cover all our needs, it sure looks good relative to the $87 million budgeted in the current two-year cycle.”

The Legislature has fooled around with the kicker before. In 1991 and 1993, budget problems relating to Ballot Measure 5 of 1990 prompted lawmakers to suspend the kicker, withholding $246 million from taxpayers. Then, in 2007, lawmakers succeeded in diverting funds from the corporate kicker to a surplus account called the rainy day fund.

Public resistance to diversion of the kicker has historically been strong. As one current Reddit post says, “The Oregon State government is run as efficiently as an HOA. The kicker policy at least mandates them to return surpluses rather than letting this group of clowns spend it on whatever is fashionable and keeps them in office.”

There’s also long been suspicion that free-spending Democrats will take undue advantage of any relaxation in kicker policy.“This past session, I was approached multiple times by Democrats who wanted to use the kicker for some purpose, and their requests were well over $10 billion,” Senate Minority Leader Tim Knopp, R-Bend, told OPB in 2023. “The reason I haven’t done any of that is, once you open the door, you’re going to spend it all.”

For all its screw-ups, Oregon is damn good at one thing, raising taxes and fees.

One of the newest gambits, SB 687, would actually remove voters from the decision-making process. Sponsored by State Senator Sen. Khanh Pham, D-Portland, and State Representatives Mark Gamba, D- Milwaukie and Zach Hudson, D – Troutdale, Wood Village, Fairview and North Gresham, the bill would allow a city or county to enact a fuel tax without going to voters first, eliminating a current requirement that local voters must approve city or county gas tax increases.

I guess in the sponsors’ view, voters just get in the way of sound policymaking.

In a classic political gaffe, Gamba has already insulted voters, going so far as to tell OPB that voters too often act like “petulant children” standing in the way of taxes that are necessary to replace vital infrastructure like roads, sewage plants and libraries. “Someone needs to be the responsible adult in the room,” he told OPB.

Oregon‘s tax system already ranks in the bottom half of states, coming in 30th overall on the 2025 State Tax Competitiveness Index and Portland enjoys the distinction of having the highest combined local income tax rate in the nation (4 percent), adding an extra layer of tax burden for residents of the state’s largest city.

You may be thankful Oregon forgoes a sales tax, but the Competitiveness Index points out it doubles down on other forms of taxation. The state has a complex and progressive individual income tax system with four tax brackets, a top marginal rate of 9.9 percent, and a personal exemption structured as a tax credit. Additionally, the tax brackets are not adjusted for inflation.

The absence of a sales tax in Oregon is offset, the Index says, by an overly complex corporate tax system, which includes a 7.6 percent corporate income tax, a 0.57 percent gross receipts tax (the Corporate Activity Tax), and additional corporate taxes at the local level, particularly in the Portland area. Although gross receipts taxes typically do not allow any deductions from gross sales, the CAT provides a 35 percent deduction for either labor costs or the cost of goods sold. However, this does not significantly improve Oregon’s competitiveness in attracting businesses, as the state’s corporate tax system ranks among the worst in the nation, comparable to Delaware, the only other state to combine corporate income and gross receipts taxes.

Oregon’s property tax system is moderately competitive, the Index acknowledges,though the property tax burden relative to personal income is higher than in California and Washington. Additionally, the state imposes an estate tax with a maximum rate of 16 percent and the lowest estate tax exemption among states that levy the tax ($1 million), which further reduces the state’s competitiveness for high-net-worth individuals.

But what do the Democrats in the Legislature care? They have a supermajority in both the Oregon House and Senate, so they’ll be able to increase taxes and fees without a single Republican vote. The hell with ordinary voters, I guess.

Like a casino that changes the Blackjack odds by shifting from one hand-held deck to multiple decks, critics of Oregon’s kicker law are preparing for a stealth raid on your wallet.

State economist, Carl Riccadonna, hired in August by Gov. Tina Kotek, “has taken it upon himself to get the forecast more in line with reality” KGW reported in November. In other words, to try to minimize (or eliminate) it.

“I think that the truing up of the calculation under the new chief economist is really going to be helpful to provide stability when we are trying to do budgeting every two years, ” Kotek said in November.

The Oregon Legislature passed the “Two percent kicker” law in 1979. It requires the state to refund surplus revenues to taxpayers when actual General Fund revenues exceed the forecast amount by more than two percent. The personal income tax kicker money comes from all state General Fund revenue sources, except for corporate tax revenues. Personal income tax is the largest contributor. In 2000, voters acting on a legislative referral put a large portion of the 2% surplus kicker statute into the state constitution (Article IX, Section 14).

In October 2023, the Oregon Office of Economic Analysis (OEA) confirmed a $5.61 billion revenue surplus in the 2021-2023 biennium, triggering a tax surplus credit, or kicker, for the 2023 tax year. The surplus—the largest in state history[1]—was returned to taxpayers through a credit on their 2023 state personal income tax returns filed in 2024.

Democrats, never at a loss for ideas on how to spend more government money, in league with unions and liberal special interest groups, are eager to see the kicker refunds throttled.

Because the kicker is in the Oregon Constitution, a ballot measure would need to be referred to the people to get them to surrender their Kicker refund, but don’t put it past the Democrat-dominated legislature to get creative to facilitate higher government spending.

“Oregon’s inaccurate revenue forecasting costs billions needed for critical public services,” said a memo Service Employees International Union Local 503, Oregon’s largest public-sector union, sent recently to Gov. Kotek.

SEIU research director, Daniel Morris, has complained that poor economic forecasting has resulted in too much money going out the door as kicker refunds. “Over the last five forecasts it’s been embarrassingly bad,” he told OPB. “There are real consequences for the families of Oregon.”

Joe Baessler, interim executive director of American Federation of State, County and Municipal Employees Council 75, has lambasted the kicker as well. “They’re deciding to under-inflate our revenue,” said Baessler. “It forces budgeting that is not in line with how much revenue is coming into the state and rolls back the amount of money we have for services that Oregonians want.”

The Oregon Center for Public Policy regularly rails against the kicker too. “Oregon’s kicker is a policy that worsens income inequality, racial inequality and geographic inequality,” says the Center.

With a new state economist committed to forecast reform, Democrats holding a supermajority in the Oregon House and Senate, Tina Kotek serving as governor, and special interest groups salivating over a bigger state budget, the generous kickers of the past are in jeopardy. Count on it.

Gov. Kotek has apparently decided not to immediately pursue multiple money-raising proposals put forward by her Housing Production Advisory Council to address the affordable housing crisis in Oregon. But you have to wonder, who are these people and what in God’s name were they thinking? How could they have been so oblivious, so tone-deaf to, the public mood?

Oregonians are in no mood for massive tax hikes, particularly to pay for more wasteful programs run by a parasitic government determined to hoover up hard-earned private income .

The proposals in the Council’s ill-advised 20-page draft report, HPAC Policy Recommendations, all of which would have continued until sunsetting in 2032, include:

Increase all personal income tax brackets by ½ percentage point

Establish a special $1 per $1,000 real property tax assessment outside of Measure 5.

Implement a 0.5% retail sales tax

Implement a 0.5% payroll tax

Double the current state fuel tax

Targeted Measure 50 Reform:

Increase annual Maximum Assessed Value change from 3% to 5%.

Authorize voters to increase the permanent levy of their local jurisdiction.

Exempt cities and counties from compression.

Adopt Land Value Tax

Eliminate Mortgage Interest Deduction for Second Homes (i.e., abolish income tax deduction for interest paid on second homes).

Enact temporary property tax exemption for new housing at 120% AMI or below.

Reduce or Eliminate Tax Expenditures (i.e., tax exemptions) not related to housing.

Total projected ANNUAL new revenue from just the first five proposals would be $2.4 billion. If enacted in 2024, and maintained until sunsetting in 2032, they would would fill state coffers by grabbing almost an astonishing additional $27 billion from taxpayers. Measure 50 reform surely would grab millions more.

Who came up with this stuff?

The report notes that four lawmakers sat as members on Kotek’s Council:

I can understand the two liberal Democrats, given their party’s predilection for government spending.

Jama represents Oregon’s 24th Senate District, which includes parts of Multnomah and Clackamas Counties. He co-founded the Center for Intercultural Organizing, now Unite Oregon, and served as the director until 2021. He was appointed unanimously by the Clackamas and Multnomah County Boards of Commissioners to replace Shemia Fagan after she was elected Secretary of State. He won election by 58.7% in 2022.

Dexter represents Oregon’s 33rd House District, which covers the Northwest District and Northwest Heights of Portland, plus Cedar Mill, Oak Hills and most of Bethany. She was appointed in June 2020 after the death of Democrat Mitch Greenlick. She won election by 84.8% in 2022.

It’s harder to understand why Republicans Dick Anderson of Lincoln City and Vikki Breese-Iverson of Prineville signed on to the Advisory Council’s massive tax proposals, unless you accept the proposition that the two parties are actually a duopoly focused on expanding government through mock competition..

Anderson squeaked into office after the incumbent Democrat decided not to run for re–election. He defeated Democrat Melissa Cribbins in the 2020 general election by just 49.4% to 46.5%.

Breese-Iverson, who formerly served as minority leader of the Oregon House, is an even more surprising advocate of higher taxes. Her Prineville home is in conservative Sen. Lynn Findley’s district. He’s one of one of six Republican senators who might be unable to run for reelection in 2024 because of his 2023 walkout. If he doesn’t run, Breese-Iverson may run in his place.

Then there are all the gubernatorial appointees to the Council.[1] With broad experience in affordable housing, finance and architecture, and most with a long Oregon presence, you’d think they would be sensitive to the public mood. They weren’t.

The reality is that the optimism and liberal tolerance so long present in Oregon has been degrading for quite a while.

A January 2022 statewide survey conducted by the Oregon Values and Beliefs Center found Oregonians questioning government spending, with half of respondents saying more than 44 cents of every dollar in state spending is wasted.

“We spent way too much money on programs without any evidence that those programs are SOLVING the problems they are meant to address,” said one male respondent aged 45-54in Multnomah County. “It seems that spending money is seen as a solution, but it isn’t. I want problems SOLVED andthen the program must end. The programs go on forever and accomplish little, if anything.”

Young adults (18-29)—a group likely to exhibit strong support for tax increases to fund social programs—reported the highest perceived waste in the state budget of any demographic group. The median response among young adults was that a whopping 56 cents per dollar of state spending are wasted.

Liberal patience has degraded most noticeably in the Portland Metro area, where about half of Oregon’s population resides.

In a May 2023 poll carried out by GS Strategy Group for People for Portland, 75% of Multnomah County voters said homelessness in the area was “an out-of-control disaster”.

More than half (55%) said “Portland has lost what made it a special place to live”. And even worse, 65% agreed that elected officials in the Portland area were listening to “a small group of insider political activists” on important issues, rather than the public at large.

The erosion of once reliable liberal tolerance for the homeless and community crime was also evident in the overwhelming support (67%) for compelling drug addiction and mental health treatment for people in crisis.

Similar shifts in public mood were evident in a December 2023 survey of Portland voters by DMH Research for the Portland Police Association. About two-thirds of respondents said the city was on “the wrong track” and more than half said they would leave if they could afford to. Almost 70 percent of those surveyed said the city was “losing what made it special” and only about 20% said the city’s best days lie ahead.

Against this backdrop, the members of the Housing Production Advisory Council were way off track in their revenue-raising proposals. Simply put, they clearly failed to “read the room” .

_____________

Gubernatorial appointees to the Housing Production Advisory Council

Ernesto Fonseca is the CEO of Hacienda Community Development Corp., which provides affordable housing, homeownership support, economic advancement and educational opportunities.

Elissa Gertler, former executive director of the Northwest Oregon Housing Authority, is Clatsop County Housing Manager, leading the county’s efforts in developing more affordable housing.

Riley Hill is a longtime local contractor in Eastern Oregon and former Ontario mayor from 2019 to 2022.

Natalie Janney is Vice President at Multi/Tech Engineering, which designs subdivision and multi-family projects throughout Oregon.

Robert Justus was co-founder of housing company Home First. With its development partners, the company has built 1,425 units of affordable housing with a development cost of more than $381 million. Justus stepped away from the company at the end of 2023.

Joel Madsen is Executive Director at Mid-Columbia Housing Authority and Columbia Cascade Housing Corporation. Both work towards promoting and administering affordable housing in the Columbia River Gorge.

Ivory Justice was selected as Executive Director of Home Forward, Oregon’s largest provider of low-income housing, in January 2023. She previously worked as Chief Executive Officer for Columbia Housing and Cayce Housing in South Carolina.

Erica Mills is Chief Executive Officer at NeighborWorks Umpqua in Roseburg. The private non-profit works with residents in Coos, Curry, Douglas, Jackson and Josephine Counties on affordable housing development, education, training, and homeowner assistance as well as lending, loan servicing and other financial services.

Eric Olsen is the owner of Monmouth-based Olsen Design and Development, Inc., a design-build land development company focusing on small to midsize projects with emphasis on residential.

Gauri Rajbaidya is a principal at Portland-based SERA Architects.

Karen Rockwell has been Executive Director with the Housing Authority of Lincoln County since late 2022. She served previously as Executive Director of Benton Habitat for Humanity in Corvallis, a commissioner on the Linn Benton Housing Authority and as vice chair of the Corvallis Housing and Community Development Advisory Board.

Margaret Van Vliet is a Portland-based consultant focusing on strategy development, organizational improvement and project management. Her specialties are housing homelessness and wildfire recovery.

Justin Wood is a Portland developer and vice president of Fish Construction NW Inc.

That was one of the recommendations of Gov. Tina Kotek’s Portland Central City Task Force convened to consider the city’s most challenging problems and recommend ways to address them.

“Declare a moratorium on new taxes…” urges the Task Force report. “…elected officials should consider a three-year pause, through 2026, on new taxes and fees…”

Oh well, so much for that.

Your Portland property taxes, which were due Nov. 15, probably already went up and will likely go up again in 2024. According to the Lincoln Institute of Land Policy and the Minnesota Center for Fiscal Excellence, Portland ranked fifth highest nationally for effective property tax rate — a homeowner’s tax bill as a percentage of a property’s value — on a median-value home in 2022.

And Portland Commissioners Dan Ryan and Rene Gonzalez are already floating a November 2024 ballot measure that would raise property taxes to cover a $800 million bond for maintenance and new construction projects for the city’s parks and fire departments.

Oregonians are also already paying higher gas taxes. Oregon’s gas tax increased to 40 cents as of Jan. 1, 2024. That’s an increase of two cents per gallon from last year. The new rate keeps Oregon among the ten states in the U.S. with the highest gas taxes. Propane and Natural Gas Flat Fee increases also went into effect for qualified vehicles on Jan. 1.

Portlanders (and many more folks) are also facing increases in electricity rates. PGE customers can expect to pay 18% more on their power bills starting Jan. 1. The 2024 rate increase will cost the average single-family household an extra $24.59 each month.

And then there are all the taxes and fees the 2003 Legislature gleefully enacted.

According to the Taxpayer Association of Oregon, Oregon lawmakers passed 185 fee increases (increasing existing fees and establishing new fees) in 2023 that will mean $47 million in higher costs.

Of those, 77 new or increased fees will directly impact the cost of medicine, hospitals and health care, which are all already straining the budgets of Oregonians. Another 47 fee increases will impact Oregon’s agriculture industry and consumers.

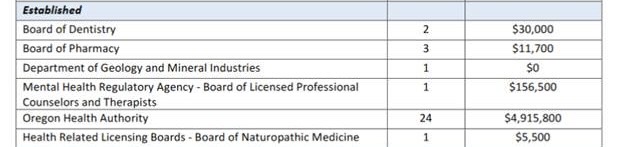

A list of 2024 fee increases by agency is below:

And then there are the new fees the 2023 Legislature created:

Portlanders and almost all Oregonians are also going to be paying a new cell phone tax this year. Starting January 1, 2024, a 988 Coordinated Crisis Services Tax will be added to the existing Oregon Emergency Communications (911) Tax. The new tax was implemented by the Oregon Legislature with the passage of House Bill 2757. The $50 million a biennium tax is slated to fund the state’s new 9-8-8 suicide prevention hotline.

DMV fees have gone up, too, touching just about everybody with a vehicle. For example:

Class C driver license or restricted Class C driver license, increased from $54 to $58

Commercial driver license, increased from $75 to $160

Instruction driver permit, increased from $23 to $30

Commercial learner driver permit, increased from $23 to $40

Hardship driver permit application, increased from $50 to $75

Fee for renewal of a commercial driver license, increased from $55 to $98

Fee for knowledge test for a motorcycle endorsement, increased from $5 to $7

Fee for a skills test for any commercial driver license, increased from $70 to $145

And the list of fee increases goes on, nickeling and diming Oregonians.

And of course legislators are busy thinking of new taxes.

For example, because the Oregon Department of Forestry wants more money to fight wildfires, Sen. Elizabeth Steiner, D-Portland, wants to charge every property owner in the state an annual fee to pay for what she perceives as a statewide issue.

And then, of course, there’s always inflation. It has been pushed down by aggressive Federal Reserve action, but in its long-term economic projections from December, the Federal Open Market Committee forecasted core Personal Consumption Expenditures Price Index inflation will drop from 3.2% in 2023 to 2.4% in 2024 and 2.2% in 2025.

But, still, hold on to your wallet. The state is considering tolls on I-205, I-5, U.S. 26 and Highway 217.

Multnomah County Democrats, who have probably never found a tax they didn’t like, are supporting a new capital gains tax on county residents, further burdening an already overtaxed populace.

People who take the time to read their voters pamphlet for the May 16, 2022 election will see Multnomah County Ballot Measure 26-238, “Eviction Representation for All”. The measure would create a program that would provide “free, culturally specific and responsive legal representation, with translation, to persons sued in Multnomah County residential proceedings (including post foreclosure) as well as related housing claims and appeals, including to maintain public housing assistance.”

The program would be funded by a new, adjustable 0.75 % tax on net capital gains of county residents. The tax rate could be increased or decreased based on the county’s annual reports.

In other words, the new tax revenue would pay for lawyers to help people fight with property owners.

Minimizing evictions may be a worthy goal, but not every social problem should generate a new tax on already burdened taxpayers. A realignment of priorities would be preferable

Without a doubt, this measure is a disaster in the making.

Although advocates argue the measure would only tax individuals, not businesses, that’s a fiction. As a study done by Perkins & Co for the Portland Business Alliance concluded, “Businesses organized as pass-through entities such as a sole proprietorship, partnership, limited liability company (except those electing to be taxed as a C corporation), and S corporation are taxed at the individual level. The majority of Multnomah County small business owners reflect the annual activity of their businesses on their individual income tax returns.”

Someone selling their business in Multnomah County would also have to pay the capital gains tax with no other investments to offset any gains.

The Perkins & Co report also noted that “taxpayers would be subject to this tax even if they were otherwise nontaxable for federal, Oregon, and other local tax purposes. “ For example, retirees withdrawing from their retirement investment accounts might not be subject to federal or Oregon income taxes, but they might have to pay could pay have to pay Multnomah County’s capital gains tax on their savings , reducing their retirement income if their withdrawals are categorized as capital gains.

Equally disturbing, Perkins & Co. concluded that homeowners selling their residence at a profit would owe the proposed local capital gains tax on all gains from the sale.

The Cascade Policy Institute has rightly pointed out another flow in the measure — the 0.75 % tax rate is adjustable. “Most of us have been around long enough to know that when a tax rate is adjustable, the only way is up,” Cascade says.

Resident small business owners in Multnomah County already face a barrage of taxes, resulting in the second highest marginal individual income tax rate in the United States after New York City, and has suffered population losses in each of the past two years. Piling on with yet another poorly designed tax would compound the county’s problems.

I guess it wasn’t enough for Democrats to allow people in the country illegally to get Oregon driver’s licenses, ignoring voters who soundly rejected the practice in 2014. Oregon’s Democrat-controlled 2019 Legislature also voted to bury Oregonians in a deluge of tax increases.

“Only time will tell whether there will be political consequences for Oregon Democrats who enacted this tax hike, Patrick Gleason, Vice President of State Affairs at Americans for Tax Reform, wrote in Forbes. “What is certain is that Oregon lawmakers are making their state a less attractive place to do business, create jobs, invest, and raise a family, and they are doing so at a time when other states are implementing reforms to make their tax and regulatory climates more welcoming.”

At the top of the 2019 Legislature’s tax list is the gross receipts tax on sales inside the state’s borders that exceed $1 million, whether or not the business makes a profit. The tax, equivalent to a sales tax, is expected to raise $2 billion per biennium. The legislative revenue office says the tax will hit about 40,000 businesses. This less than three years after almost 60% of Oregon voters rejected Measure 97, a ballot measure that would have imposed a state gross receipts tax.

Adding insult to injury, the Democrats passed SB 116 setting a particularly inconvenient election date if a tax repeal petition now seeking signatures qualifies for the ballot. Rather than having the vote take place during the general election in 2020, when there’s likely to be high interest and participation, the bill provides for a special election on January 21, 2020.

I guess they figured picking Christmas or New Year’s Day for the vote would be too obvious an attempt at manipulation.

Paid Family Leave legislation (HB 2005-B) is going to cost you, too. A 1% payroll tax will fund a paid family leave insurance program (FAMLI) to be administered by the Oregon Employment Department. The tax will come on top of the business sales tax.

A Revenue Impact statement projected that employers will pay $542.3 million and employees $1,029.6 in 2021-2023. In 2023-2025, employers will pay $ 775.0 million and employees $1,471.5 million.

Then there’s the maneuvering with the kicker. The collective “kicker” tax rebate Oregonians will likely receive when they file in 2020 is going to be $108 million smaller, thanks to HB 2975, a bill Gov. Kate Brown signed into law in April.

And don’t forget SB 861, which provides for paying the postage for election ballots. It will cost taxpayers an estimated $1.7 million per election. Gov. Brown pushed for the law, figuring it would increase voter turnout. In a rather bizarre statement, given the widespread availability of stamps, Brown testified that low-income and younger residents don’t always have access to postage stamps.

There’s also HB 2449-B, a 50-cent increase in the emergency communications tax on our phones, which will bring the total to $1.25 per month.

Oregon’s minimum wage law is increasing employer costs, too.

According to the Office of Economic Analysis Department of Administrative Services, the law will result in a slowdown in job growth. “While the impact is small when compared to the size of the Oregon economy, it does result in approximately 40,000 fewer jobs in 2025 than would have been the case absent the legislation,” the office has reported. “Our office is not predicting outright job losses due to the higher minimum wage; however, we are expecting future growth to be slower as a result.”

And next year, Oregon voters will get a chance to vote on an increase in yet another Oregon tax, this one on tobacco. If approved, the cigarette tax would increase by $2 a pack and E-cigarettes and cigars would be taxed at 65% of their wholesale price.

Whew, what a torrent!

As the humorist Gerald Barzan observed, “Taxation with representation ain’t so hot either.”

Charities and much of the media are screaming bloody murder about the potential negative impacts of the new 503-page tax reform legislation.

“The tax code is now poised to de-incentivize the heart of civic action in America,” Dan Cardinali, president of Independent Sector, which represents charities, told the Washington Post.

“The GOP tax reform will devastate charitable giving,” shrieked the Los Angeles Times.

Stacy Palmer, Editor of “The Chronicle of Philanthropy,” said on Public Television’s Newshour that as much as $20 billion might not be given in 2018 next year because of the tax law change. An Indiana university study estimated the reduction would be $13 billion.

This apocalyptic vision fits in nicely with the attempt by Democrats to demonize the tax reform law and the Republicans who voted for it in hopes of reaping benefits in the 2018 elections.

But is charitable giving really going to implode? I think not.

The primary concern among the nattering negative cadre appears to be that the number of Americans who qualify for the charitable tax deduction will drop sharply now that the standard deduction has been doubled to $12,000 for an individual, $24,000 for couples. This will result in fewer people itemizing their deductions, and you can only deduct donations if you itemize, a key factor motivating charitable giving, according to the doomsayers.

But this ignores the fact that an awful lot of people already give generously from the heart without claiming a charitable deduction. According to the most recent IRS data, 68.5 percent of households chose to take the standard deduction under the old system, leaving them unable to claim a charitable deduction, but a lot of them made donations anyway. In 2016, the largest source of charitable giving was individuals at $281.86 billion, with two thirds of households giving money to non-profits.

It is estimated that under the new tax law, the share of people itemizing deductions could drop to as few as 5 percent.

It seems highly unlikely that individuals who haven’t been itemizing or those who won’t itemize under the new tax system will decrease their charitable giving when the standard deduction is doubled. In other words, the vast middle class will still probably give, though charities may want to ramp up their appeals.

What looks considerably more threatening for charities is changes in the estate tax under tax reform.

Before the tax reform law, the estate tax applied only to estates worth at least $5.49 million for individuals and $10.98 million for married couples. The estate tax applied a 40 percent tax rate to estates worth more than those amounts.

In other words, the wealthy have been encouraged to make charitable donations because these donations were not taxed. If their money was left to heirs instead, the estate would pay taxes on amounts greater than about $5.5 million dollars for an individual or $11 million for a couple.

The new tax law tax doubles the annual exclusion amount (the exemption) for estate taxes to $10 million. Couples who do proper planning could double that exemption.

Only 0.2% of all estates ended up being hit with the estate tax under the old formula. The Tax Policy Center estimates that some 11,310 individuals dying in 2017 will leave estates large enough to require filing an estate tax return.

Under the new law, it’s likely that fewer than 1,000 estate tax returns will be filed per year with a tax due. In other words, just 10,000 individuals may be less likely to make charitable donations to avoid estate taxes.

But those individuals control a lot of wealth and many may be people who were previously motivated to give by a desire to avoid estate taxes.

According to the National Committee for Responsive philanthropy (NCRP), study after study shows that tax policy matters in charitable giving and that the estate tax is one of the most important motivators for those at the top of the income distribution. “Rather than see a sizable portion of their estates subject to taxation, wealthy families give while living to reduce the size of their estates; and they also give in the form of bequests upon their death, “ the NCRP says.

The Chronicle of Philanthropy has compiled detailed data on publicly reported charitable gifts of $1 million or more in each state. The largest recipients include private and community foundations, colleges and universities, healthcare programs, the arts, museums and libraries. The Chronicle assumes that a large proportion of those donations is motivated by estate tax planning.

So Oregon charities relying on big gifts may be in for a harder struggle going forward.

The Chronicle data shows the following significant gifts of $1 million or more to Oregon institutions just in 2017 and 2016: